-

青色専従者給与とは?「専ら従事」の意義について判断基準を解説!

青色専従者給与の制度趣旨 同族会社経営者等との公平性 法人を設立して事業を営んでいる同族会社の経営者は、配偶者その他の親族を役員にするなどして役員報酬・給与を支払い、所得の分散をはかることが可能です。所得税は、個人単位の累進課税となります... -

配偶者や親族への業務委託費(外注費)は経費にできるのか?

個人事業主の配偶者や親族への支払いは原則として必要経費にできない 所得分散のために検討されることが多い 所得税は個人単位で課税され、累進課税という特徴があるため、所得分散により世帯単位での納税額を圧縮しようとする意図をもって、検討されるこ... -

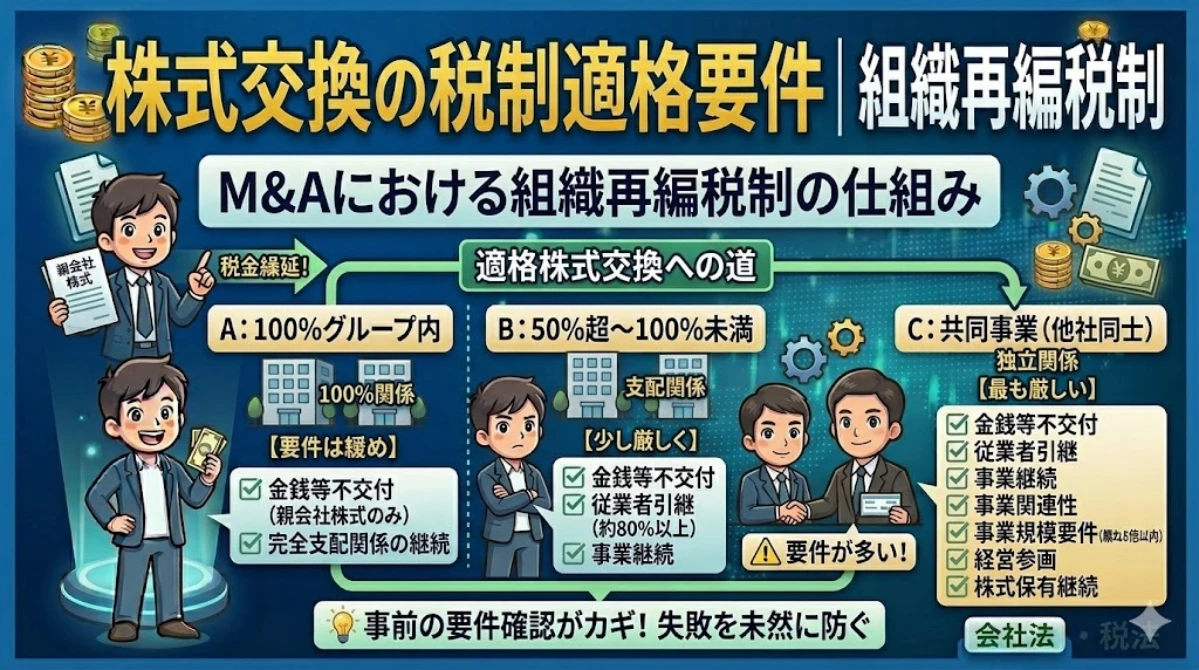

株式交換の税制適格要件 | 組織再編税制

適格株式交換の分類 適格株式交換は、次のように分類されます。 100%グループ内の株式交換 完全支配関係(株式交換後も完全支配関係が継続する見込みが必要)の企業グループ内の株式交換で、次の要件を充足すると適格株式交換に該当します。 適格株式交換... -

消費税のリバースチャージ方式とは?導入の背景からインボイスへの対応も含めて解説!

導入の背景 課税対象を定める消費税法第4条 (課税の対象) 国内において事業者が行つた資産の譲渡等(特定資産の譲渡等に該当するものを除く。第三項において同じ。)及び特定仕入れ(事業として他の者から受けた特定資産の譲渡等をいう。以下この章に... -

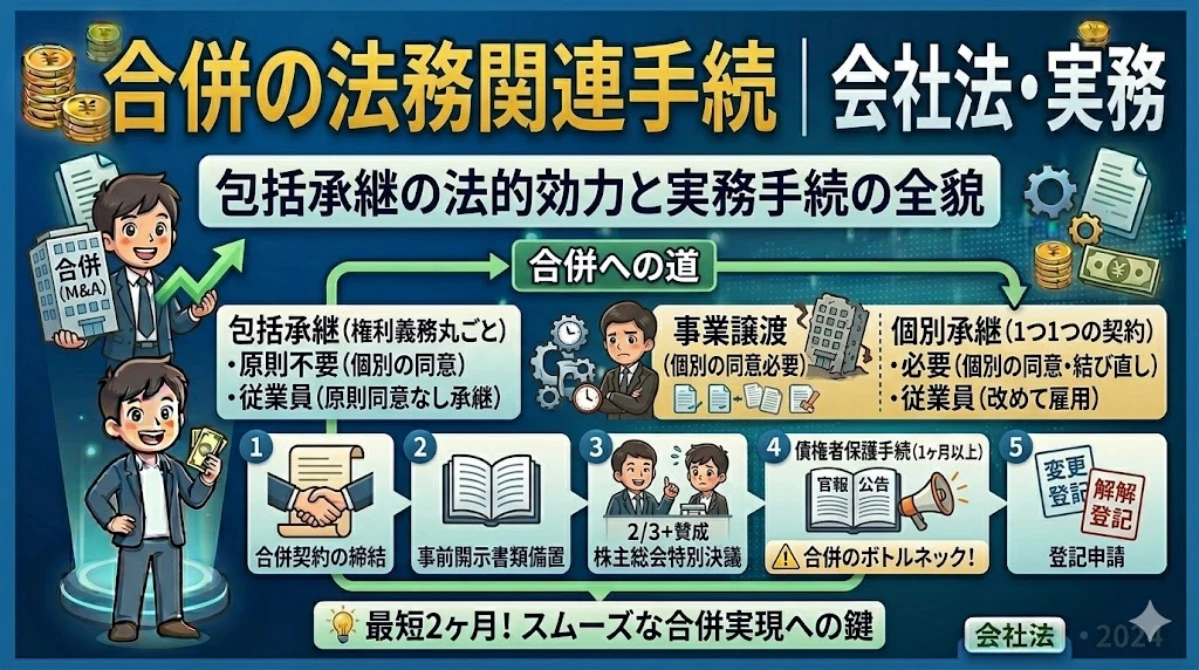

合併の法務関連手続 | 会社法

手続の概要と趣旨 株主への影響 合併は、異なる企業が統合されることになるため経営環境に大きな影響を与えます。そのため、原則として株主総会の決議により株主の承認を得ることが求められております。 合併に反対する株主が存在する中で合併が実施される... -

公認会計士事務所と税理士事務所の違いとは??受託できる業務の違いから特徴を解説!

独占業務と事務所の呼称 企業運営に伴って生じる委託業務とは 会社を設立するなどして事業を開始すると、士業に依頼しなくてはならない業務が多々生じます。 会社運営に伴い発生する主な士業への依頼業務 税務 給与計算 社会保険手続(健康保険、厚生年金... -

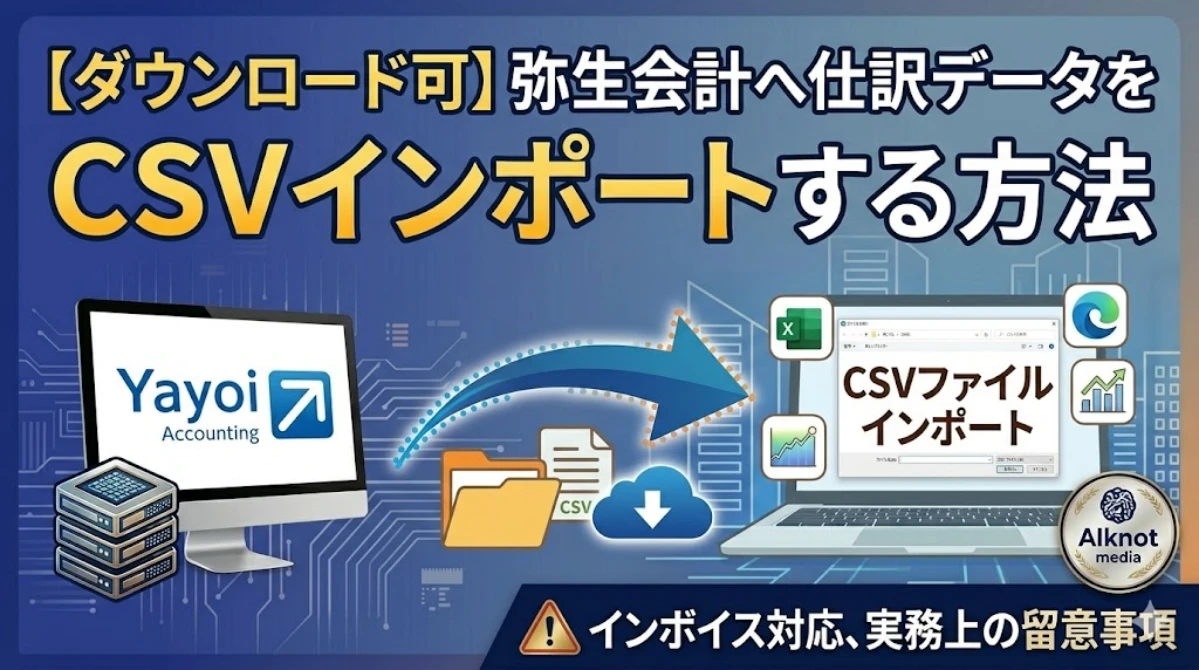

【ダウンロード可】弥生会計へ仕訳データをCSVインポートする方法

まず所定様式に合わせてフォーマットを作成する 公式のひな形がない? 最近の会計ソフトはクラウド型が主流になってきているため、大量の仕訳を手入力するには適しておらず、その場合、エクセルファイルによるインポートが推奨されていることが多くありま... -

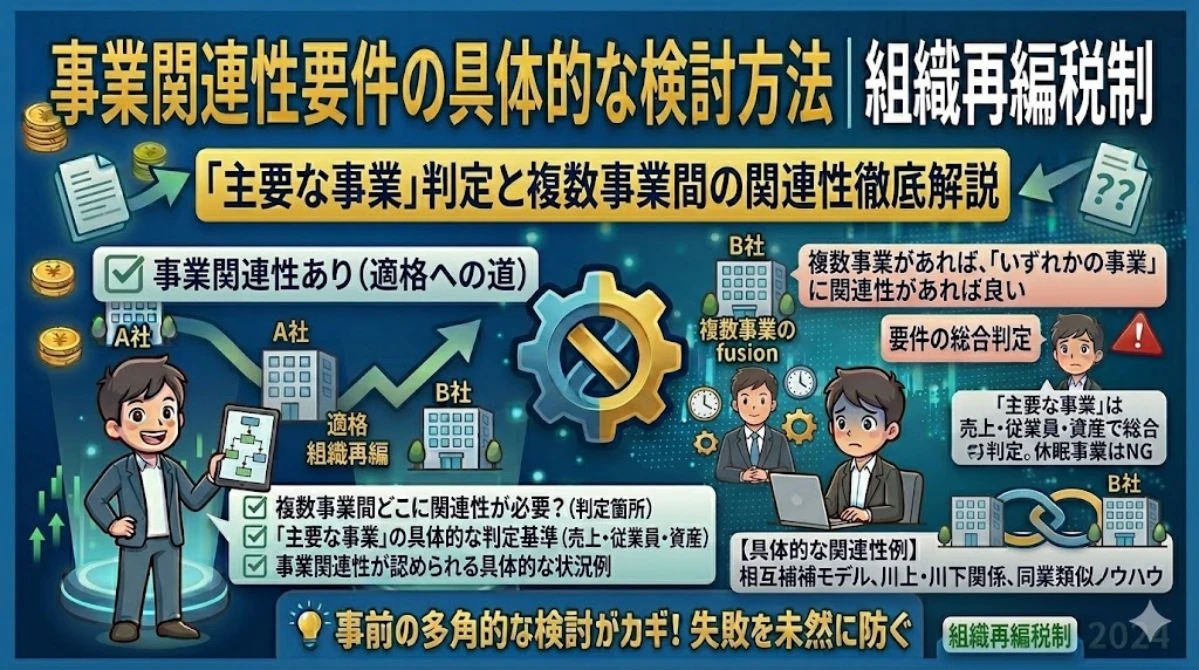

事業関連性要件の具体的な検討方法と留意点 | 組織再編税制

適格要件充足のための具体的検討事項 関連性が求められる事業の範囲 合併の場合 合併を例に取ると、被合併法人の主要な事業と、合併法人のいずれかの事業に事業関連性があれば要件を充足いたします。やや分かりにくいですが、表にまとめると次の通りです。... -

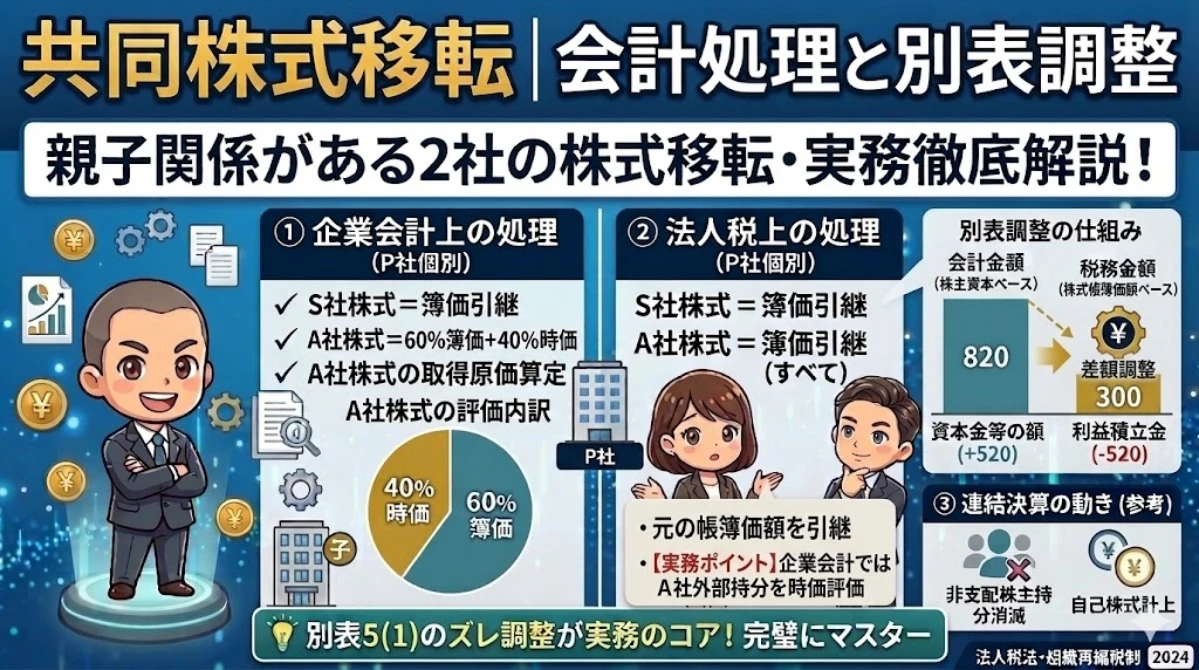

共同株式移転 – 会計処理と別表調整 | 非支配株主が存在するケースについて連結も含めて解説!

事案の概要 (例)S社はA社議決権の60%を保有していた。S社とA社は、株式移転により株式移転設立完全親会社P社を設立した。 図:株式移転の全体像 ・交換比率は1:0.5・取得企業はS社と判断された・S社株主はS社株式を帳簿価額200で保有している... -

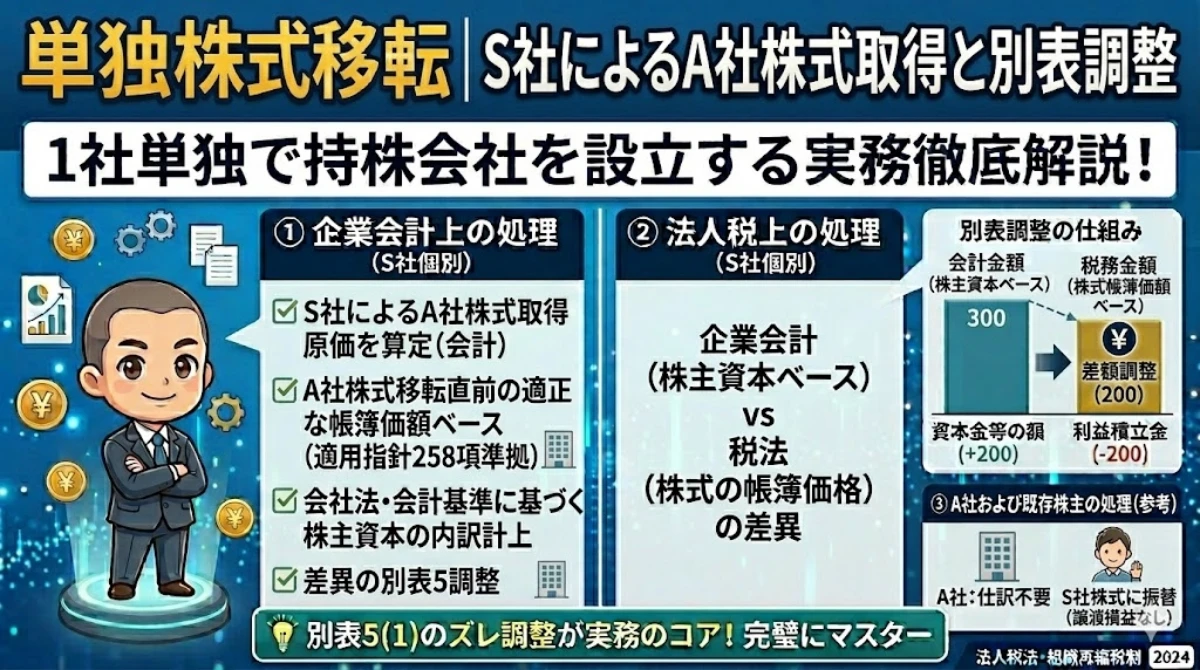

単独株式移転‐会計処理と別表調整 | 単独企業が持株会社を新設するケースについて解説!

事案の概要 (例)P株主はA社の発行済株式の100%を保有していたが、株式移転により持株会社となるS社を設立した。 図:株式移転の全体像 ・共通支配下の取引に該当する・適格株式移転に該当する・P株主はA社株式を帳簿価額100で保有している・S社は...