-

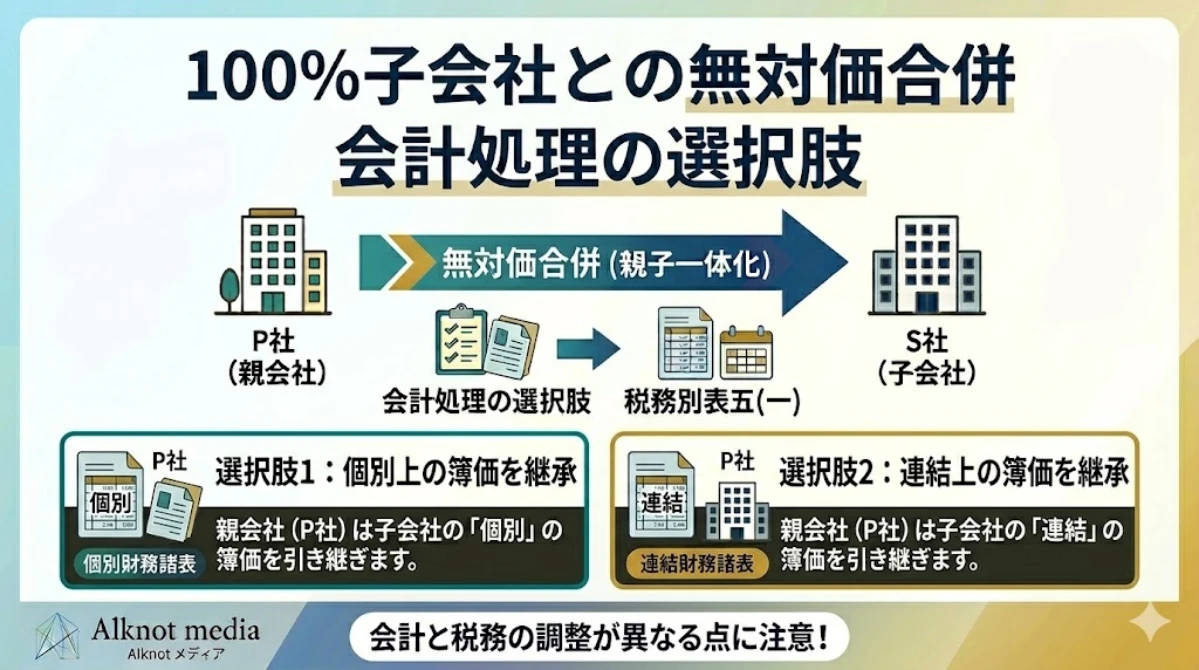

100%子会社との無対価合併ー会計処理と別表調整 | 単体・連結・税務

会計上の処理 具体例の概要 (例)P社は、×1年度末にS社の100%を取得して完全子会社とし、×2年度末にS社を無対価合併いたしました。 図:組織再編関係 図:S社のタイムテーブル 適格合併に該当する のれんの償却年数は5年 ×1年度末に純資産300のS社... -

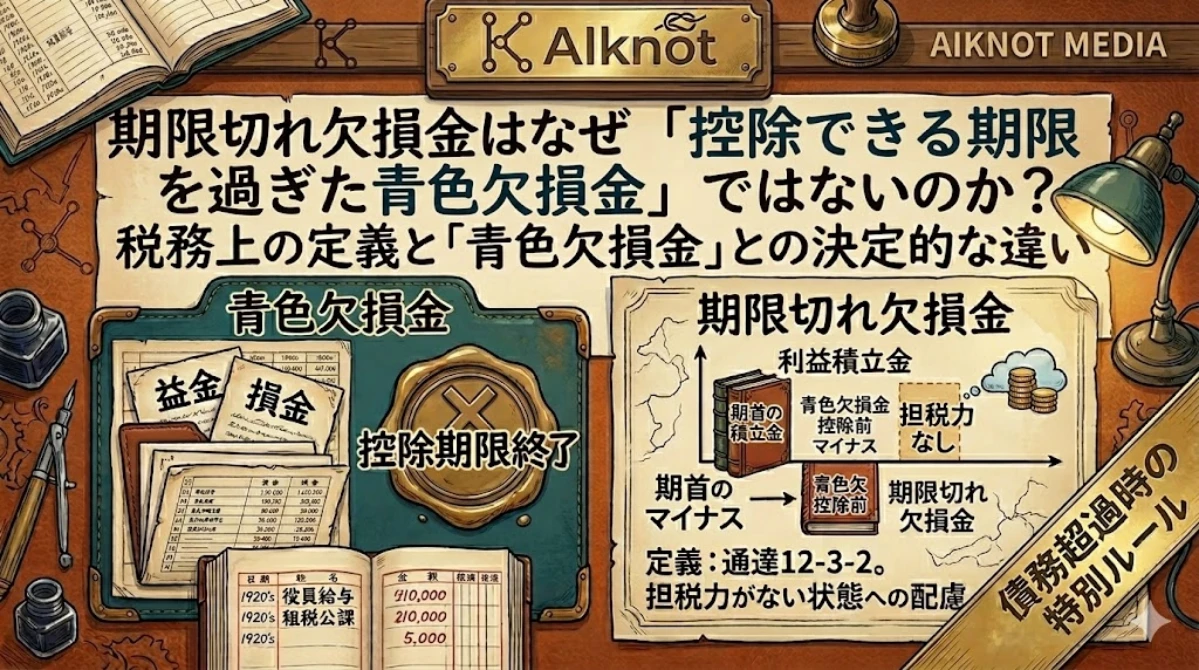

期限切れ欠損金はなぜ「控除できる期限を過ぎた青色欠損金」ではないのか

期限切れ欠損金に見る青色欠損金との制度趣旨の違い 清算や再生の局面で利用できる「期限切れ欠損金」とは 期限切れ欠損金という語感から、別表7で控除されることなく失効した過去の青色欠損金のことであると感じられます。しかし、通達により期首のマイ... -

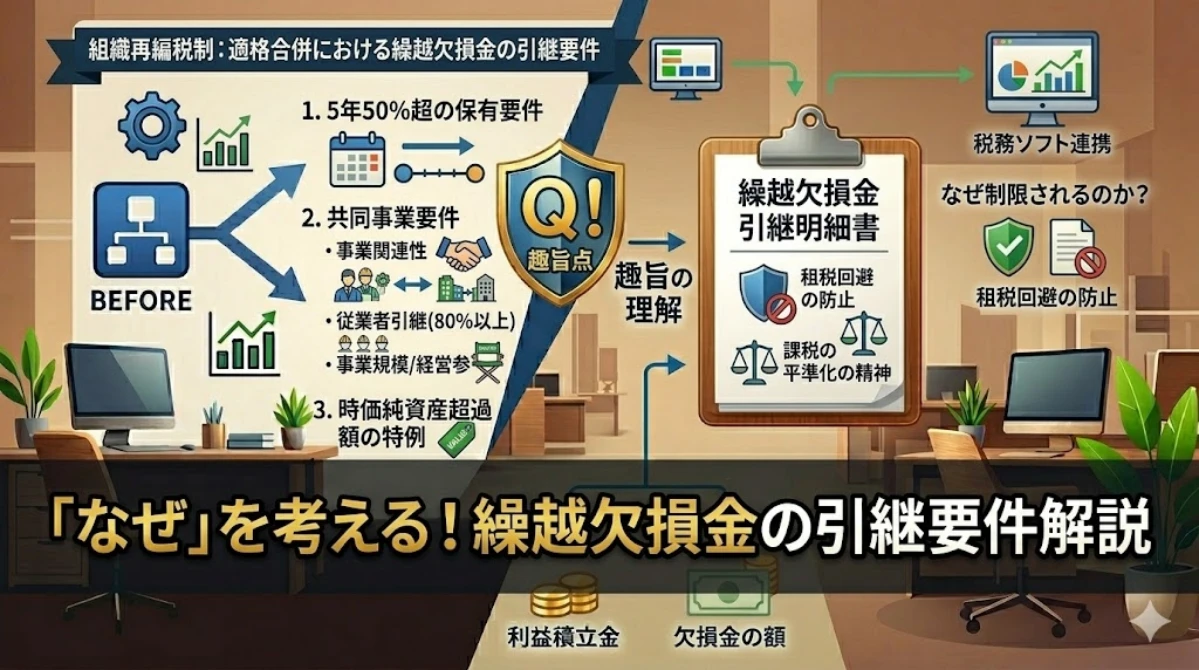

適格合併における繰越欠損金の引継要件の何故を考える | 組織再編税制

適格合併における繰越欠損金の引継ぎ制限とは 引継ぎ制限が生じないための要件 一定の要件のいずれかを充足しない限り、適格合併において繰越欠損金の引継ぎに制限が生じます。組織再編の形態により変化いたしますが、概ね下記の要件に整理することができ... -

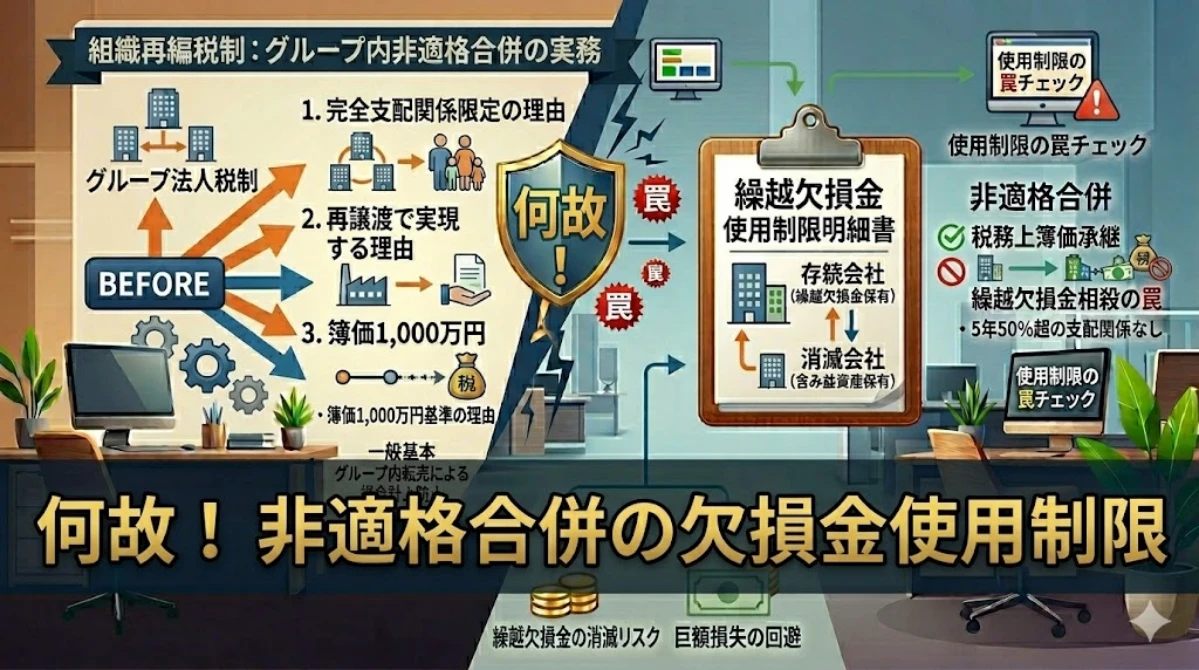

グループ法人税制の意義から「非適格合併により生じる繰越欠損金の使用制限」の何故を考える | 組織再編税制

グループ法人税制の意義とは グループ間の売買による損金計上を防止するための規定 バブルの崩壊による土地価格の下落を初めとして、資産の含み損が生じると、その含み損の実現により税金を減少させようという誘因が生じます。経済的実態として含み損が実... -

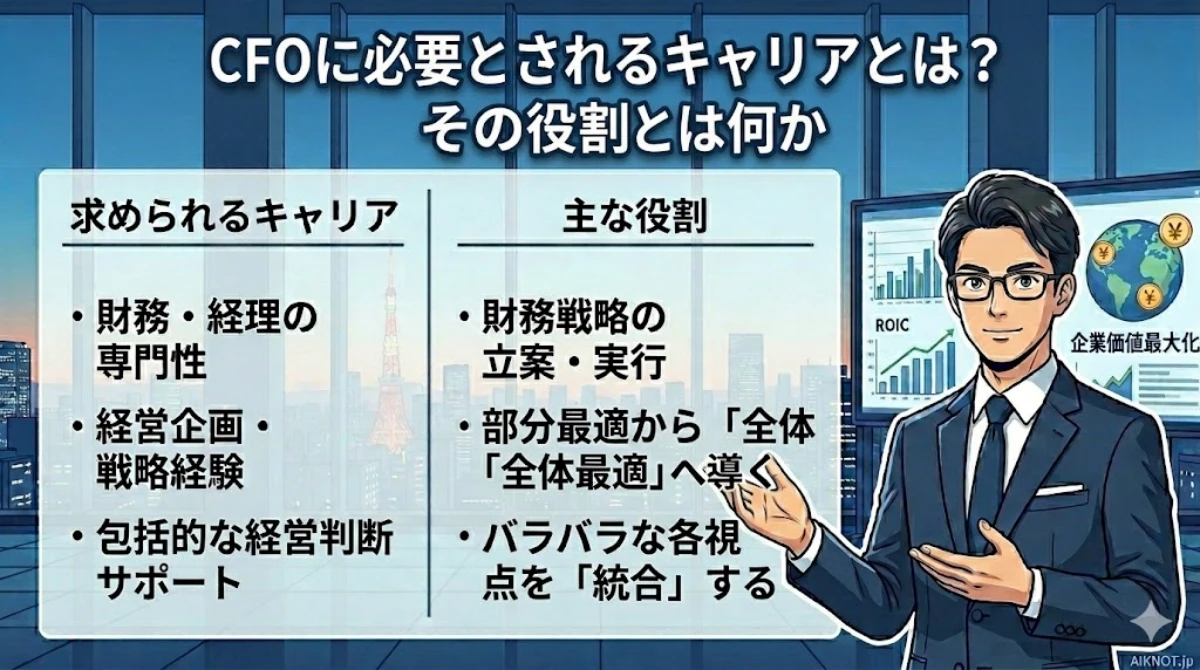

CFOに必要とされるキャリアとは?その役割とは何か

企業においてCFOが必要とされる理由 日本CFO協会が定めるCFOの役割と存在意義 一般社団法人日本CFO協会では、CFOの存在意義と役割について以下のように記載されております。 企業価値の向上を図ると共に、世界の基準に合わせた透明性を確保する財務管理力... -

多くのIPO準備企業で上場延期の原因に!早めの対応が必須なIPOに向けた労働時間の管理とは?

90%以上が改善を求められる労働時間の管理体制 監査法人の監査よりも主幹事証券の審査の方が厳しい領域に該当 監査法人による会計監査、内部統制監査は、あくまでも財務諸表に対して心証を得ることを目的としています。そのため、財務諸表に計上した財務数... -

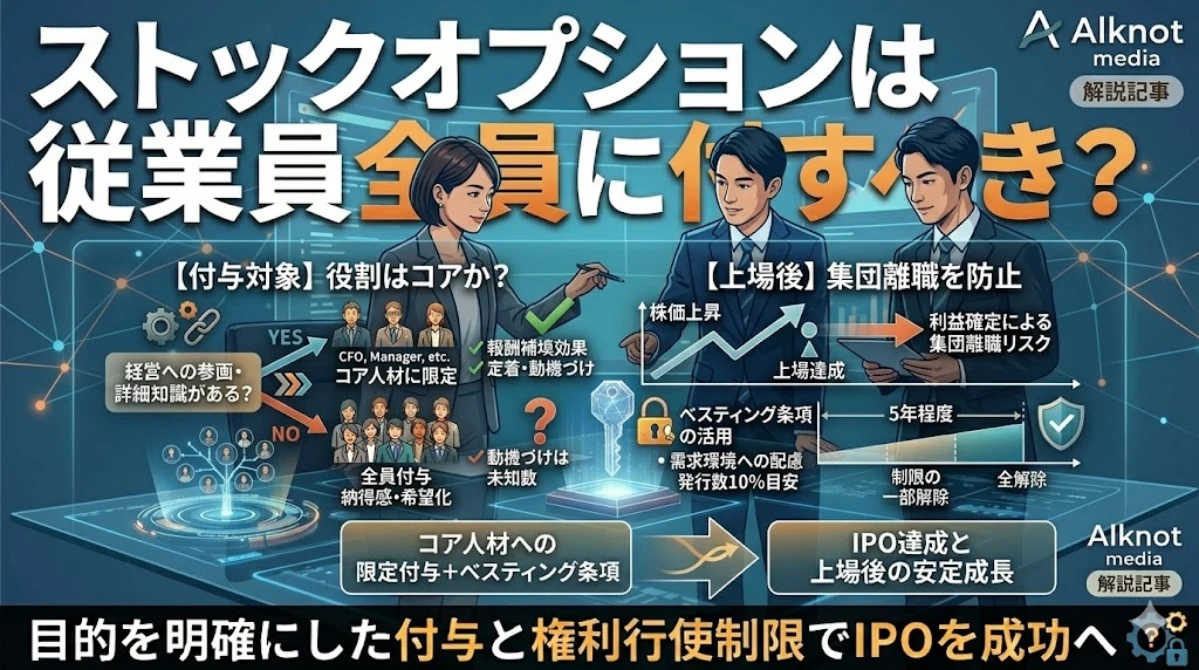

ストックオプションは従業員全員に付すべき?

ストックオプションの失敗例は多い 何のためにストックオプションを付すのかを明確にする IPO準備において、ストックオプションの付与は広く行われています。ただ、場合によっては大きな所得をもたらすこともあり、付与の仕方によっては従業員が不満を感じ... -

資本政策のバリュエーションは高い方がいいのか?

高くするデメリットもある 初回の資金調達で高くしてしまいがち どの企業も、ほとんどが序盤は単一の株主しかいません。そのため、いざ増資によって資金調達をしようとする際に、過度に高いバリュエーションを提出してしまうことが多くあります。少ない株... -

会計freeeが使いにくいと感じる理由

現金主義採用の傾向が強い freee請求書から連携される仕訳に感じるfreeeの考え方 freeeの凄い点は、スモールビジネス向けに、かつては大企業しか導入できなかったERPを提供したことです。インターネット環境の発展を存分に活用してこれを実現しており、マ... -

IPOにおける資本政策の税務上の留意点

資本政策には事前の計画が大切 資本政策の目的 何故、資本政策の作成を行い、計画的に実施することが大切なのでしょうか。それは、資本取引を行う時期や順番に間違えてしまったがために大きな損失を被ってしまったり、資金繰りが回らなくなってしまること...